The 60-40 Investment Strategy: A Time-Tested Approach

The 60-40 investment strategy, a cornerstone in the world of finance, has long been revered for its simplicity and effectiveness. At its core, this strategy revolves around allocating 60% of an investment portfolio to stocks and the remaining 40% to bonds. But what makes this seemingly straightforward allocation so special? Let’s delve deep into its historical significance, the underlying principles, and the reasons behind its widespread adoption.

Historical Significance of the 60-40 Strategy

The origins of the 60-40 strategy can be traced back to the early days of modern portfolio theory. Financial experts recognized the need for a balanced approach that could offer both growth potential and a safety net. By combining the high-reward, high-risk nature of stocks with the stability of bonds, investors could achieve a harmonious balance.

The Basic Premise: Diversification Through Stocks and Bonds

Stocks: The Growth Engine

Stocks, representing ownership in a company, offer the potential for significant returns. They are influenced by company performance, industry trends, and broader economic factors. However, with higher potential returns comes higher volatility, making them a riskier asset class.

Bonds: The Stability Anchor

Bonds, on the other hand, are essentially loans made by investors to entities (like governments or corporations). In return, these entities promise to pay periodic interest and return the principal amount at maturity. Bonds are generally considered less volatile than stocks and provide regular income, making them a preferred choice for risk-averse investors.

Why 60% Stocks and 40% Bonds?

The 60-40 split isn’t arbitrary. This specific allocation was found to offer an optimal balance between risk and reward for a broad range of investors. The 60% allocation to stocks provides ample exposure to the growth potential of equities, while the 40% allocation to bonds offers a buffer against the inherent volatility of the stock market.

The Traditional Appeal of the 60-40 Mix

The 60-40 investment strategy has, for decades, been the bedrock of many portfolios, offering a blend of growth and stability. But what exactly is the allure of this mix? Why has it stood the test of time, and how do stocks and bonds traditionally complement each other? Let’s explore these questions and more.

The Yin and Yang of Stocks and Bonds

Much like the ancient Chinese philosophy of Yin and Yang, where seemingly opposite forces may be complementary and interconnected, stocks and bonds in the 60-40 mix often work in tandem to balance a portfolio.

Stocks: The Upside Potential

Stocks, being equity instruments, give investors a stake in a company. When the company performs well, its stock price generally rises, leading to capital appreciation. Additionally, many companies distribute a portion of their profits as dividends to shareholders, providing an income stream.

Bonds: The Counterbalance

Bonds act as the counterweight in this mix. When the stock market is turbulent, bonds, especially those from stable governments or blue-chip companies, tend to remain steady or even appreciate. This is because bonds are seen as safer havens, and their fixed interest payments offer predictability in uncertain times.

Economic Slowdowns and Their Impact

Economic slowdowns or recessions can be challenging times for stock markets. Companies might see reduced profits, leading to declining stock prices. However, during these times, central banks often intervene.

Central Bank Interventions

Central banks, like the Federal Reserve in the U.S., might cut interest rates during economic downturns to stimulate borrowing and investment. When interest rates are cut, bond prices typically rise. This is because existing bonds with higher interest rates become more attractive compared to new bonds issued at the now-lower rates.

| Economic Condition | Stock Market Reaction | Bond Market Reaction | Central Bank Action |

|---|---|---|---|

| Growth | Positive | Neutral/Mildly Negative | May raise interest rates |

| Recession | Negative | Positive | Likely to cut interest rates |

The Diversification Benefit

The main reason the 60-40 mix has been so popular is the diversification benefit it offers. When stocks decline, bonds often rise (and vice versa), ensuring that the overall portfolio doesn’t see extreme swings. This balance means that the overall risk of the portfolio is less than the sum of its parts.

Historical Performance: A Testament to Resilience

Historically, the 60-40 mix has shown resilience across various market cycles. Even during periods of stock market downturns, the presence of bonds has cushioned portfolios, leading to smoother returns over time.

Challenges in the Modern Economy

The 60-40 investment strategy, while historically robust, faces new challenges in today’s rapidly evolving economic landscape. From the aftermath of global events like the pandemic to the changing role of bonds, the traditional pillars of this strategy are being tested. Let’s delve into these modern challenges and their implications for the classic 60-40 mix.

Post-pandemic Dynamics and Their Impact

The global pandemic brought unprecedented challenges to economies worldwide. With businesses shuttering, unemployment rates soaring, and global trade disrupted, the stock markets experienced significant volatility.

Central Bank Responses

To combat the economic downturn, central banks globally adopted ultra-loose monetary policies, slashing interest rates to historic lows and pumping trillions into the economy. While these measures provided short-term relief, they also had long-term implications.

- Stock Market: With cheaper borrowing costs and a flood of liquidity, stock markets rebounded sharply from their March 2020 lows. However, this rapid ascent raised concerns about overvaluation and potential bubbles in certain sectors.

- Bond Market: The bond market faced a dual challenge. Low interest rates meant lower yields for new bonds. Additionally, with inflation concerns on the horizon due to massive fiscal stimulus, the real returns on bonds (returns after accounting for inflation) became even more compressed.

The Changing Role of Bonds as Diversifiers

Traditionally, bonds have been viewed as the stabilizing force in a 60-40 portfolio. However, with interest rates at or near zero in many developed economies, the cushioning effect of bonds is diminished.

- Diminished Returns: With low yields, the income-generating potential of bonds has reduced. This challenges the 40% allocation in the traditional mix, as investors seek better returns elsewhere.

- Inflation Concerns: As governments rolled out massive stimulus packages, concerns about rising inflation emerged. Inflation erodes the purchasing power of fixed interest payments from bonds, making them less attractive.

Seeking Alternatives to Traditional Bonds

Given the challenges with traditional government bonds, investors are exploring alternatives:

- Corporate Bonds: These offer higher yields compared to government bonds but come with increased credit risk.

- Emerging Market Bonds: Bonds from emerging economies can offer attractive yields, but they carry higher geopolitical and currency risks.

- Inflation-Linked Bonds: These bonds offer protection against inflation, as their interest payments rise with increasing inflation.

The Inflation Factor

Inflation, often termed the “silent thief,” erodes the purchasing power of money over time. For the 60-40 investment strategy, understanding the implications of inflation is crucial, as it directly impacts both stocks and bonds. In this section, we’ll explore how persistent inflation can alter monetary policy dynamics and its potential impact on the traditional stock-bond relationship.

Understanding Inflation

Inflation represents the rate at which the general level of prices for goods and services rises, causing the purchasing power of currency to decline. While moderate inflation is considered normal in growing economies, hyperinflation or prolonged high inflation can be detrimental.

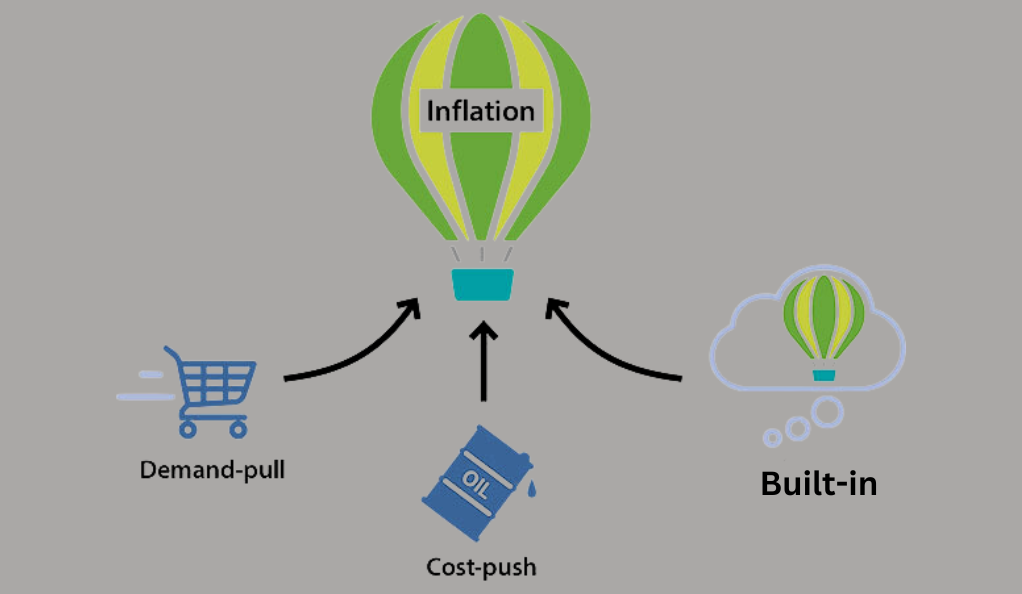

Causes of Inflation

- Demand-pull inflation: Occurs when demand for goods and services exceeds their supply.

- Cost-push inflation: Arises due to increased costs of production, leading to higher prices for consumers.

- Built-in inflation: Results from the interplay between worker wage demands and company price increases.

Inflation’s Impact on the 60-40 Strategy

Effect on Stocks

- Eroding Purchasing Power: As inflation rises, consumers’ purchasing power diminishes, leading to reduced consumer spending. This can negatively impact company revenues and profits.

- Benefit for Debt-laden Companies: Companies with significant debt can benefit from inflation if they borrowed money at fixed interest rates. The real value of their debt decreases as inflation rises.

Effect on Bonds

- Reduced Real Returns: The fixed interest payments from bonds lose value in real terms during high inflation periods. This makes bonds less attractive as the real yield (nominal yield minus inflation) diminishes or even turns negative.

- Interest Rate Risks: Central banks may hike interest rates to combat high inflation. When interest rates rise, bond prices fall, leading to capital losses for bondholders.

Monetary Policy Dynamics in the Face of Inflation

Central banks use monetary policy as a tool to control inflation. Key actions include:

Raising Interest Rates: By making borrowing more expensive and saving more attractive, central banks can reduce money supply and curb inflation.

Selling Government Securities: By selling bonds, central banks can absorb excess money from the financial system.

Adapting the 60-40 Strategy for Inflationary Environments

In the face of inflationary challenges, investors could contemplate strategies such as leaning towards real assets, including real estate or commodities, which often retain value during inflationary periods. Additionally, they might consider integrating inflation-protected securities, like the U.S. Treasury Inflation-Protected Securities (TIPS), which adjust their principal value in line with inflation.

Rebuilding Resilience: The Need for Alternatives

The 60-40 investment strategy, while historically effective, is facing new challenges in today’s complex financial landscape. With diminishing bond yields and heightened stock market volatility, there’s a growing need to explore alternative assets to maintain portfolio resilience. In this section, we’ll delve into the increasing challenges faced by the 60-40 portfolio and introduce the concept of alternative diversifiers.

The Evolving Challenges of the 60-40 Mix

The traditional appeal of the 60-40 strategy lies in its ability to balance growth (stocks) with stability (bonds). However, several modern challenges are testing this balance:

- Persistently Low Bond Yields: Central banks’ accommodative monetary policies have led to historically low interest rates, reducing the income potential of bonds.

- Stock Market Overvaluations: With abundant liquidity and low-interest rates, there are concerns about potential overvaluations in certain stock market sectors.

- Geopolitical Risks: From trade wars to regional conflicts, geopolitical events can introduce sudden and significant volatility.

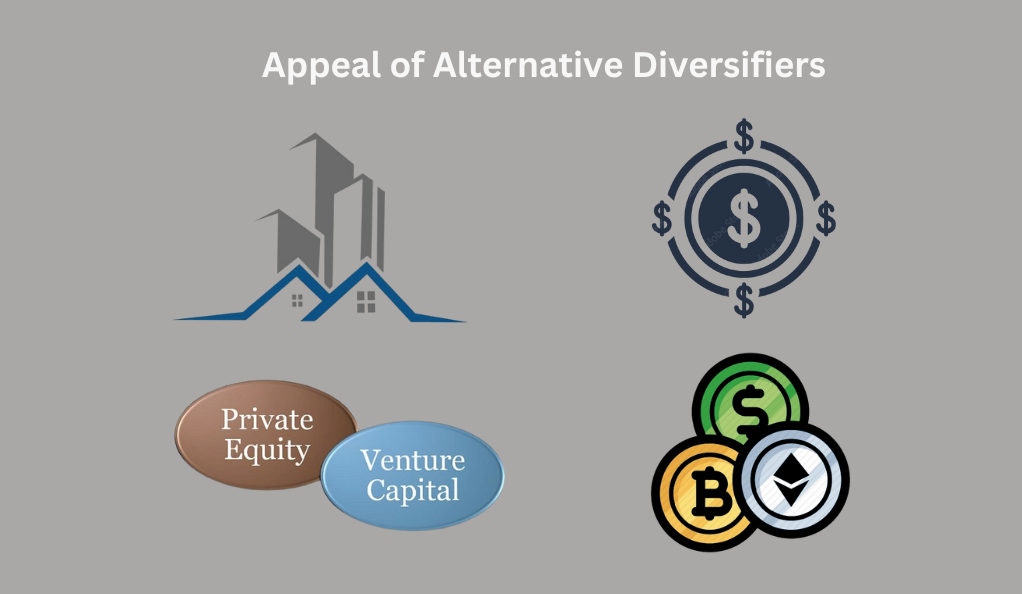

The Appeal of Alternative Diversifiers

Given these challenges, there’s a growing interest in alternative assets that can provide diversification benefits, potentially enhancing returns and reducing portfolio volatility.

Real Assets

Assets like real estate, commodities, and infrastructure can act as a hedge against inflation and provide diversification benefits. Their returns often have low correlations with traditional stocks and bonds.

Private Equity and Venture Capital

Investing in private companies or startups can offer higher potential returns than traditional public equities. However, they come with higher risks and reduced liquidity.

Hedge Funds

These pooled investment funds can employ a range of strategies, from long-short equity to global macro, offering diversification and potentially uncorrelated returns.

Cryptocurrencies

Digital assets like Bitcoin and Ethereum have gained attention as potential diversifiers. While they offer significant return potential, they also come with high volatility and regulatory uncertainties.

Long/Short Strategies: A Closer Look

One of the popular alternative strategies is the long/short equity approach. Here’s a brief overview:

- Objective: To achieve positive returns regardless of market direction.

- How It Works: Fund managers take long positions in stocks they expect to rise and short positions in stocks they expect to fall. The goal is to profit from both upward and downward market movements.

- Benefits: Potential for positive returns in both rising and falling markets, reduced portfolio volatility, and enhanced diversification.

Dispersion: A New Perspective

In the realm of investment strategies, dispersion is an often-overlooked concept that can offer unique insights and opportunities. As the traditional 60-40 strategy faces challenges in the modern financial landscape, understanding and leveraging dispersion becomes increasingly relevant. In this section, we’ll explore what dispersion means, its significance, and how it offers a form of return that might be overlooked by the traditional 60-40 construct.

What is Dispersion?

Dispersion, in the context of finance, refers to the spread of returns among assets in a particular category or market. It measures the degree to which individual asset returns deviate from the overall market or category average.

Key Points:

- High dispersion indicates a wide range of returns, with some assets significantly outperforming or underperforming the average.

- Low dispersion suggests that most assets are delivering returns close to the market average.

Why Does Dispersion Matter?

Dispersion offers insights into market dynamics and potential investment opportunities:

- Indicator of Market Sentiment: High dispersion can indicate a lack of consensus among investors about the future prospects of assets, leading to varied performance.

- Opportunity for Active Managers: In periods of high dispersion, skilled active managers can potentially identify and capitalize on mispriced assets, aiming for outperformance.

- Risk Management: Understanding dispersion can help investors gauge the potential risk and volatility in their portfolios.

Dispersion in the Context of the 60-40 Strategy

The conventional 60-40 strategy, centered on capturing broad market trends, could fail to consider the subtleties of dispersion. This phenomenon holds significant implications for the strategy: within the realm of stocks, a high dispersion environment can lead to pronounced outperformance or underperformance by specific sectors or companies, thereby introducing a dual prospect of opportunities and equity-related hazards. On the bonds front, divergence in bond yields takes on particular significance, particularly within a varied bond market featuring government, corporate, and high-yield bonds. Such yield dispersion not only offers insights into credit risks but also provides a window into prevailing market sentiment.

Harnessing Dispersion for Enhanced Returns

To leverage dispersion effectively, investors can consider:

- Sector Rotation: Shifting allocations to sectors that show promising return potential based on dispersion metrics.

- Diversified Bond Exposure: Exploring different bond categories, from government to high-yield, to capture varied yield dispersions.

- Active Management: Engaging with investment managers who have a track record of successfully navigating high-dispersion environments.

The Three Ds of Alternative Diversifiers

As the traditional 60-40 investment strategy faces challenges in today’s evolving financial landscape, the search for alternative diversifiers becomes paramount. In this quest, three key principles emerge as essential considerations: Diversification, Durability, and Defensiveness. Collectively known as the “Three Ds,” these principles guide investors in evaluating alternatives for a more resilient portfolio. Let’s delve into each of these principles and their significance.

Diversification

The cornerstone of any robust investment strategy, diversification involves spreading investments across various assets or asset classes to reduce risk.

Key Considerations:

- Correlation: The degree to which two assets move in relation to each other. Assets with low or negative correlation can provide true diversification benefits.

- Asset Breadth: Expanding the investment universe beyond traditional stocks and bonds. This might include commodities, real estate, private equity, and even cryptocurrencies.

- Geographic Diversification: Investing across different regions or countries to mitigate the impact of localized economic downturns or geopolitical events.

Durability

Durability refers to the ability of an investment or strategy to withstand economic downturns and deliver consistent returns over the long term.

Key Considerations:

- Historical Performance: While past performance is not indicative of future results, understanding how an asset or strategy performed during previous market cycles can offer insights.

- Inherent Stability: Assets that have intrinsic value or stable demand, such as gold or real estate, can offer durability.

- Adaptability: Strategies or assets that can evolve with changing market dynamics, ensuring their relevance and resilience over time.

Defensiveness

Defensiveness is the ability of an asset or strategy to protect capital, especially during market downturns.

Key Considerations:

Volatility: Assets with lower volatility can offer a smoother return profile, reducing the magnitude of drawdowns during market corrections.

Income Generation: Assets that provide regular income, such as dividend-paying stocks or bonds, can offer a cushion during market downturns.

Hedging Capabilities: Some assets or strategies, like certain options or hedge funds, can act as hedges, protecting portfolios from adverse market movements.

Evaluating Alternatives with the Three Ds

When considering alternative diversifiers, it’s essential to evaluate them against the Three Ds framework:

| Alternative Asset | Diversification | Durability | Defensiveness |

|---|---|---|---|

| Real Estate | High | High | Medium |

| Commodities | Medium | Medium | High |

| Private Equity | High | Medium | Low |

| Cryptocurrencies | Medium | Low | Low |

Conclusion

The 60-40 investment strategy, a stalwart in portfolio management for decades, is at a crossroads in the face of modern economic challenges. While its foundational principles of diversification and balance remain timeless, the instruments and approaches within this strategy require reevaluation. As the financial landscape evolves, so too must our strategies, emphasizing adaptability, innovation, and a keen understanding of global dynamics. Investors who embrace these changes, while staying rooted in the core tenets of sound investing, will be best positioned to navigate the uncertainties of the future.

Bitcoin-up is dedicated to providing fair and trustworthy information on topics such as cryptocurrency, finance, trading, and stocks. It's important to note that we do not have the capacity to provide financial advice, and we strongly encourage users to engage in their own thorough research.

Read More